Interest Rates, Housing Sales and Residential Lending Forecast -- July 2020

Each month Fannie Mae and the MBA forecast interest rates, existing and new-home sales and residential lending. Freddie Mac forecasts these also, but only on a quarterly basis. The following includes only the expectations of the monthly releases from Fannie Mae and the MBA as of July 2020. Given the economic environment, the Fannie-MBA outlook for housing and mortgage lending is rather up-beat despite the Q1-Q2 recession and ongoing drag on the economy as many businesses remain throttled down due to Coronavirus.

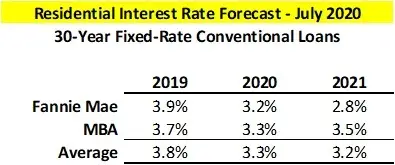

Interest Rates

Mortgage rates hit an all-time record low last week, with the 30-year fixed rate at 2.98 percent as measured by Freddie Mac’s weekly Primary Mortgage Market Survey. Fannie Mae remains more optimistic for a low interest rate environment going forward in 2021 compared to the MBA. Fannie Mae forecasts 30-year rates dipping to 2.8 percent average in 2021 contrasted to the MBA’s expectation for rates to edge up 3.5 percent.

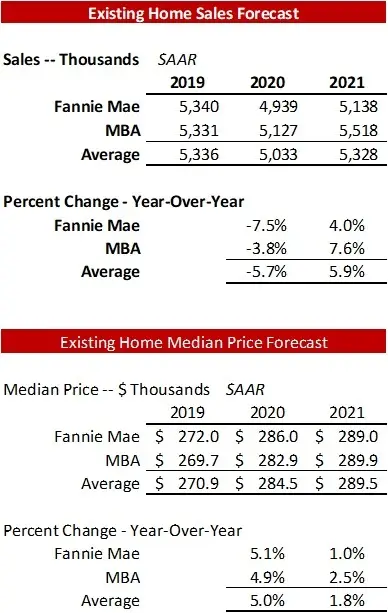

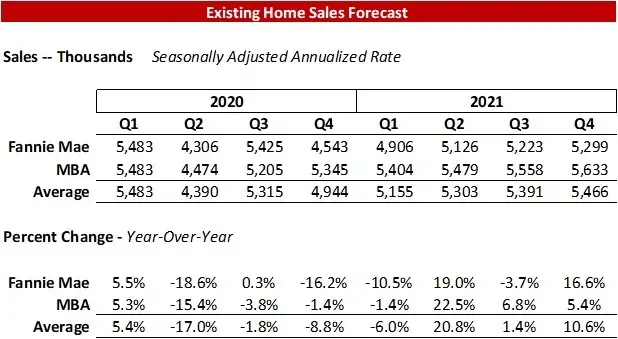

Existing Home Sales & Median Prices

The MBA remains more optimistic coming in with an estimated 3.8 percent year-over-year drop in existing home sales in 2020 vs Fannie Mae’s 7.5 percent decline. That divergent view continues into 2021, though on the upside with Fannie Mae expecting a 4.0 percent year-over-year increase and MBA almost double at 7.6 percent gain. The 5.0 percent median price gain expectation for 2020 improved from the June forecast of 3.7 percent.

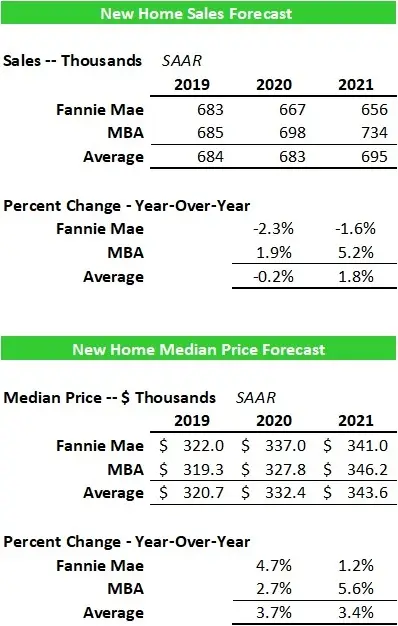

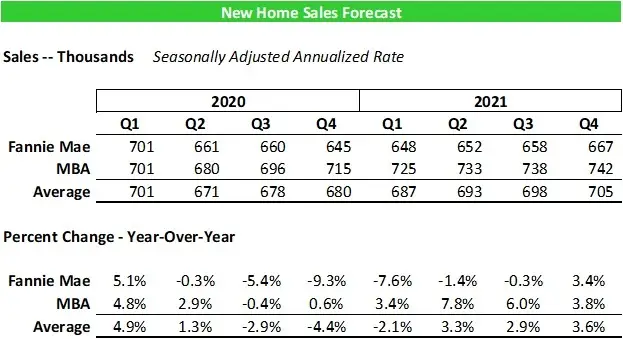

New Home Sales

New home sales in 2020 average to a no-change expectation, with Fannie coming in at roughly 2 percent down from 2019 and MBA up 2 percent. Fannie Mae sees 2021 still down 1.6 percent, but the MBA is contrarian with a 5.2 percent gain. The median new-home price is expected to rise 3.7 percent in 2020 and 3.4 percent in 2021.

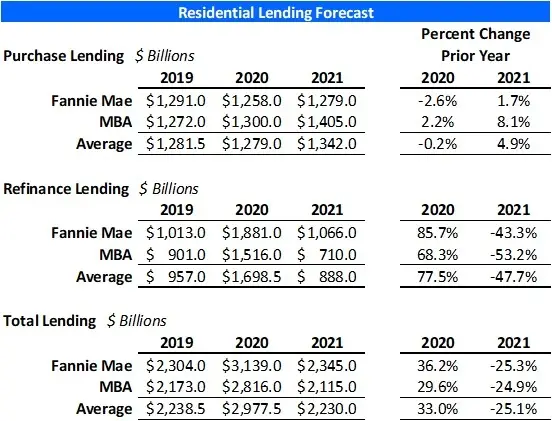

Residential Lending

The story in lending is the spike in refinance volume in 2020 driven by lower rates. The consensus is for refinance lending volume to be up 77.5 percent in 2020 but down 47.7 percent in 2021. The 2020 surge in refi will see a 33.0 percent gain in 2020 total residential lending (purchase + refi) but then slide back to the same volume seen in 2019 resulting in a 25.1 percent decline from 2020. From a business perspective, lenders will benefit from the refinancing surge in 2020, with 2021 looking like a copy of 2019.

All of this depends on jobs. The wildcard is the potential for shutdowns across the country that would drive up job losses. Uncertain is the impact of looming cuts in employment by firms temporarily able to maintain payrolls using the Payroll Protection Program, and whether or not Congress will extend these lifelines, and if so at what levels. Known are the pending cuts in the airline industry. Unknown are the potential 10s of thousands of small businesses that may shutter their doors if a recovery does not come back.

Jobs are everything.

Ted