Housing Affordability -- A Lot Better Than You Think and a PHENOMENAL 2021 Outlook

Talk to almost any homebuyer today and ask the top hurdles facing them, it is all but guaranteed that affordability hits at or near top of their list of challenges. A strong headwind for homebuyers in the past 12-months was the 11.4 percent jump in the median sales price of existing homes when comparing August 2020 ($310,600) to August 2019 ($278,800) as reported by the National Association of Realtors® (NAR).

The best year-over-year gain in median household income in the past 30 years was 8.7 percent in 2019 – and that is not likely to be repeated in 2020 given the pandemic-driven recession. The expectations are for a decline in 2020 incomes, not a gain. The official 2020 median household income will not be known until July 2021. Political Calculations 2020, a blogger on seekingalpha, has a current estimate calling for a 3.0 percent decline in median household income in 2020 to $66,627.

There are more components to affordability, however. Overall affordability of buying a home is an interaction of household income, housing prices, interest rates and the down payment. When considering all of these factors, the trend in affordability may surprise you.

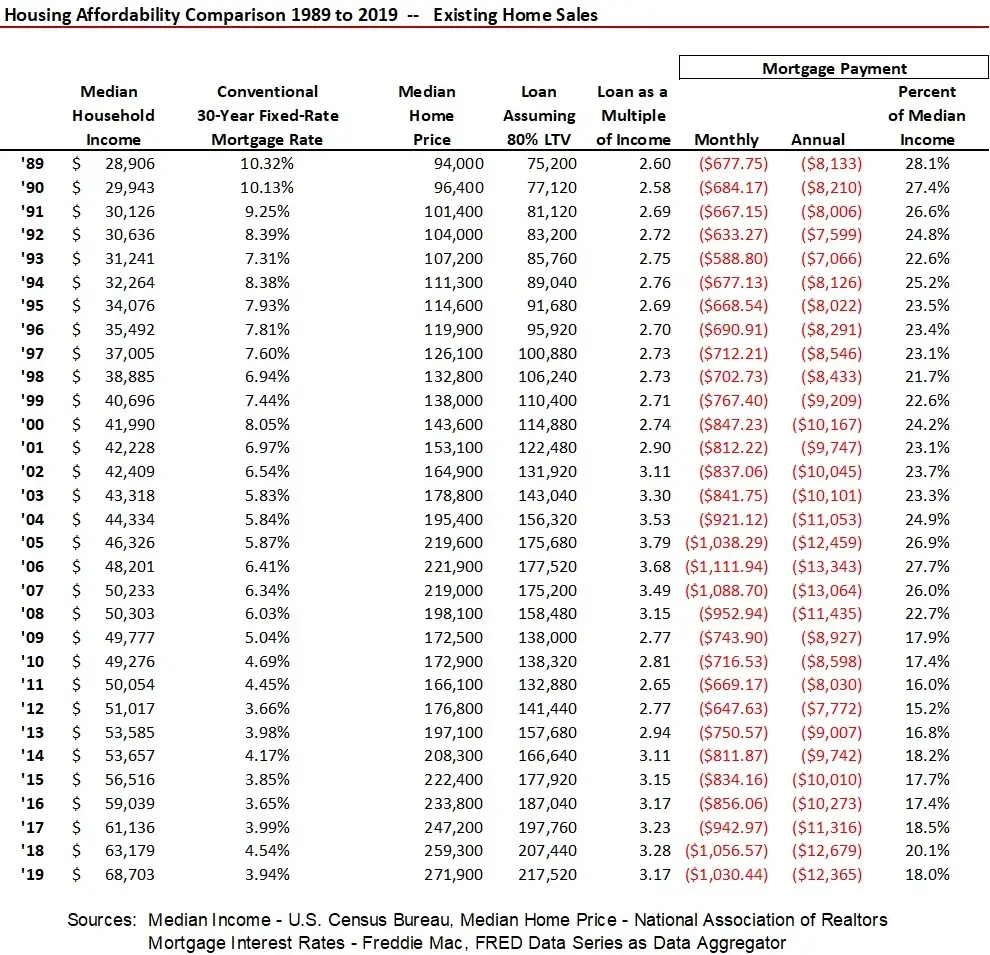

The following table looks at the affordability factors of buying an existing home annually commencing 1989. Data (all nominal) and sources include:

- Median Household Income – U.S. Census Bureau, obtained via fred.stlousfed.or

- Median Existing Home Sales Price – National Association of Realtors

- 30-Year, Fixed-Rate Conventional One-to-Four-Family Residential Mortgage Commitments – Freddie Mac, obtained via fred.stlousfed.org

The primary assumption included a 20 percent down payment (80 percent loan-to-value ratio), with monthly principle and interest payments multiplied times 12 to annualize. Property taxes and insurance were not considered – but are costs faced by all homeowners.

Findings

The first table shows the comparative affordability by year based on median household incomes and existing home prices and residential mortgages rates. For the median household to buy the median existing home in 2019 required 18.0 percent of median household income to make the annual principle and interest payments.

In the 30 years prior to 2019, just seven years required a lesser percentage of household income to make the annual principle and interest payments

The calculated monthly principle and interest payment (P&I) in 2019 of $1,030.44 was less than in 2018 at $1,056.57, 2006 at $1,088.70, 2005 at $1,111,94 and 2004 at $1,038.29

Loan amount as a multiple of median household income was greater in seven of the 30 years compared to 2019

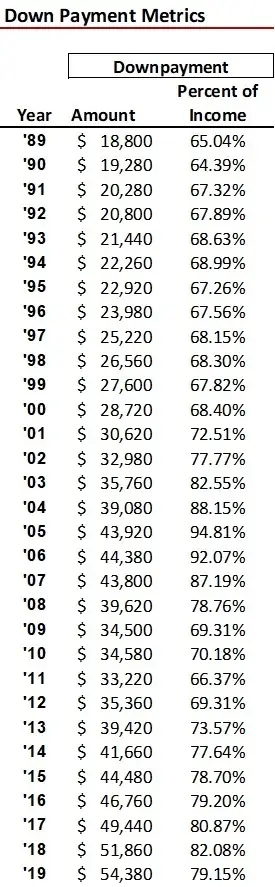

Thanks to record-low mortgage rates, the monthly P&I was low in 2019 at 18.0 of median household income, but rising price puts a burden on buyers due to a greater down payment. The next table shows the implied down payment given the 80 percent loan-to-value assumption and the corresponding percentage of the down payment to median household income. Eight of the prior 30 years required a down payment greater than the 79.15 percent in 2019. The peak was 95.8 percent in 2005 a function of madly escalating home prices during the housing bubble.

Though median household income grew at just 2.9 percent compounded annual since 1989 and median home prices at 3.6 percent, record low mortgage rates are buffering what otherwise would be deteriorating affordability.

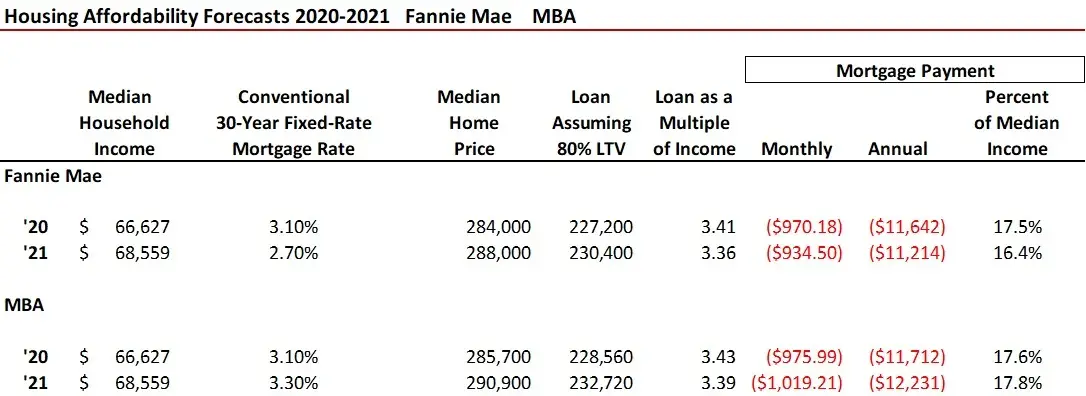

The next table uses forecasts from Fannie Mae and the MBA for median home prices and residential mortgage rates for 2020 and 2021. There is also an assumption of median household income using the seekingalpha-based estimate of $66,627 for 2020, indexed up by 2.9 percent for 2021 – the annual compound growth rate for the past 30 years. Fannie Mae shows 2020 P&I at 17.5 percent of median household income, dropping to 16.4 percent in 2021. If correct, then the P&I payments in 2021 as a percentage of median household income would be the 3rd lowest since 1989. That is incredible affordability.

The MBA is less optimistic about lower rates in 2021 forecasting a 3.3 percent average mortgage rate for the year, but that would still make it the 7th most affordable year since 1989.

Home price and household income data vary significantly with respect to location while interest rates also diverge -- but to a lesser extent (that difference was the basis of my dissertation for the PhD). Once again TINSTAANREM axiom is invoked — There Is No Such Thing As A National Real Estate Market or economy. Nor is there consistency in incomes, home prices and interest rates across states or cities. Overall, however, recent housing affordability and the outlook remains positive. When closing on the new home we had constructed in College Station, Texas, in 1989, I recall being thrilled that the 30-year fixed-rate loan was 9.75 percent – the lowest in more than a decade. At that time P&I required 28.1 percent of median household income to buy the median priced-home based on the nationwide data above. With a forward forecast for 2021 from Fannie Mae and MBA ranging from 16.4 percent to 17.8 percent of median income to service the debt, the outlook next year for housing affordability is PHENOMENAL.

Ted