Interest Rates, Housing Sales & Residential Lending Forecast 2020-2021 as of October

The increased amount of time we are spending at home makes the residence more intrinsically valuable than at any time in people’s lives today. Coupled with record-low interest rates, new and existing home sales and refinance lending volumes continue to grow – with total residential lending now forecast by Fannie Mae to hit a record high $4.083 trillion in 2020. Home sales and refinance volumes remain as key drivers of the U.S. economy today and ongoing economic recovery. Following is a summary of the October 2020 forecasts from Fannie Mae and the MBA for interest rates, existing and new-home sales and residential lending. Once again, Fannie Mae and the MBA were more optimistic in their monthly forecast as home sales and lending continue to grow.

Interest Rates

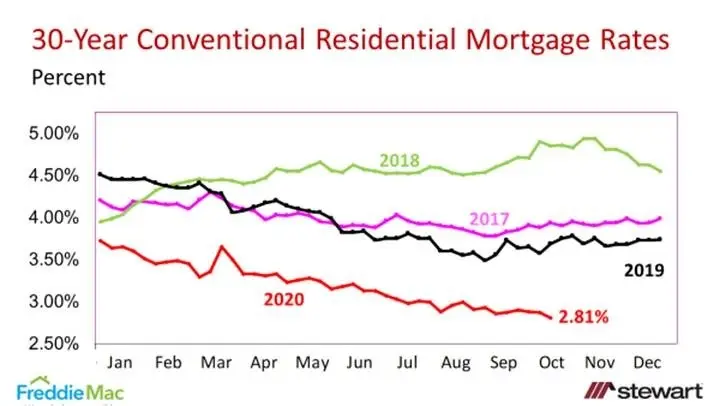

Conventional mortgage interest rates hit an all-time record-low 2.81 percent in the 3rd week of October as tracked by Freddie Mac in their weekly Primary Mortgage Market Survey. That is 88 basis points less than one-year ago, resulting in a reduction in the monthly mortgage payment per $100,000 borrowed from $459.72 to $411.43. This makes the monthly payment 10.5 percent less today than one-year ago assuming a home of equal price. Weekly 30-year, fixed-rate conventional mortgage rates since 2017 are shown in the following graph.

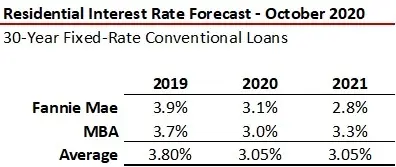

Expectations of rates for 2020 and 2021 are shown in the table. While Fannie Mae and the MBA have a similar expectation for the average rate in 2020 -- 3.0 percent to 3.1 percent -- they continue to diverge in 2021 with Fannie Mae forecasting a down tick to 2.8 percent (revised from 2.7 percent in the prior month’s forecast) and the MBA expecting rates to rise to 3.3 percent.

Existing Home Sales and Median Prices

Fannie Mae and the MBA continued to be more optimistic in their October forecast for existing home sales for 2020 and 2021. Fannie Mae changed from an expected 4.5 percent drop in their estimate as of August to essentially flat (-0.4 percent) as of the September forecast and is now at a 1.2 percent gain. The MBA moved from a 3.2 percent decline (August forecast) to no change (September) and now expect existing home sales to increase 3.6 percent in 2020. The MBA continues to be more enthusiastic for home sales in 2021 with existing home sales at the 6.1 million level (up 10.0 percent year-over-year) and Fannie Mae basically flat at 5.5 million. Average forecast increase in median home price is 6.3 percent in 2020 and 2.8 percent in 2021.

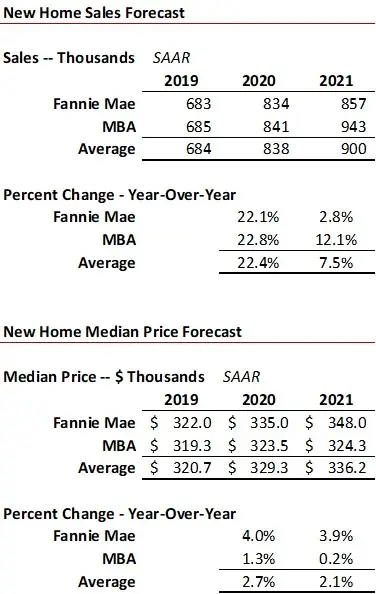

New Home Sales and Median Prices

After the best new home sales report since 2006 in August, new home sales are now forecast to be up 22 percent in 2020 and another 7.5 percent in 2021. New home median prices are forecast to rise from 1.3 percent to 4.0 percent in 2020 and from essentially flat (0.2 percent) to a 3.9 percent gain in 2021.

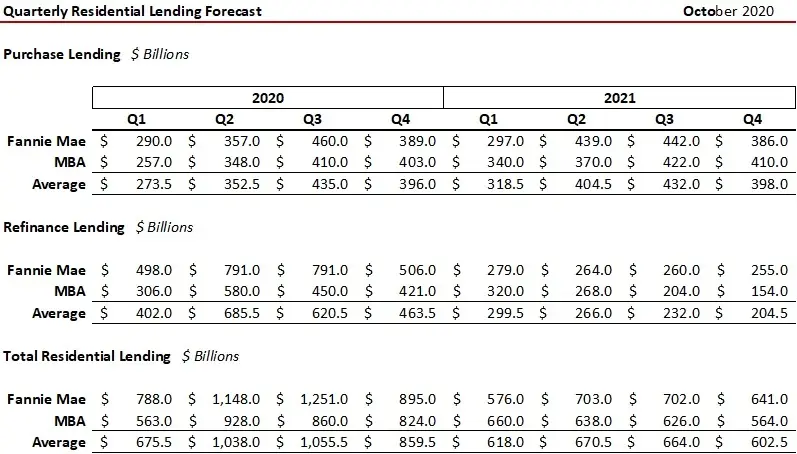

Residential Lending

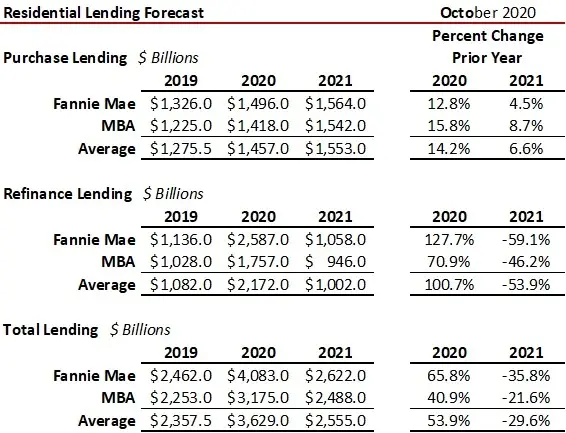

Fannie Mae is now forecasting an all-time record $4.08 trillion total residential lending volume in 2020, up from the prior record $3.76 trillion in 2003. While purchase lending is expected to rise approximately 14 percent in 2020, refinance lending will double based on the average projection, with Fannie Mae showing a 127.7 percent surge compared to 2019 and MBA up 70.9 percent. Both show an estimated halving in refinance lending volumes from 2020 to 2021.

Quarterly lending volume estimates are shown in the following table, with percentage change from the prior year in the second table.

The wildcard driving housing sales and refinance forecasts is the number of jobs. Regardless of how low interest rates go, if a prospective buyer or homeowner desiring to refinance does not have a job and a reasonable credit rating, that transaction fails to take place. Jobs are everything to the economy and to home purchases. Robust home sales and record refinance volumes would indicate that renters and not homeowners continue to shoulder the economic burden of housing arising from the pandemic. Unlike homeowners that have been protected by forbearance, renters have not been so fortunate. Eventually the impact of the expiration next year on the moratorium on evictions across renters and homeowners will be realized. The 2020 version of extend and pretend continues.

Keep an eye on unemployment statistics as they will likely be a key indicator of the U.S. housing market.

Ted