Housing Sales, Residential Lending & Interest Rate Forecasts November 2020

The latest monthly forecasts from Fannie Mae and the MBA show that the only thing the two agree on is not to agree in 2021 for either interest rates or existing home sales. Each provides a monthly prognosis on the residential housing sector including homes sales, prices, interest rates and lending.

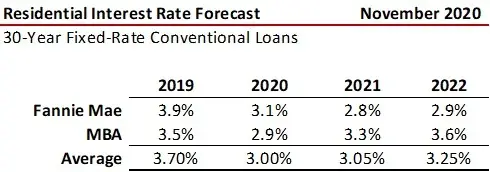

Interest Rates

Interest rates have a profound impact on housing affordability. The U.S. hit an all-time record low this month at 2.78 percent for 30-year, conventional fixed-rate mortgage loans for the week ending November 5th according to the Freddie Mac’s Primary Mortgage Market Survey. The annual average outlook for future rates from MBA and Fannie Mae are shown in the table. While Fannie thinks rates drop to 2.8 percent next year, the MBA forecasts rates will rise to an average 3.3 percent.

Existing Home Sales and Median Prices

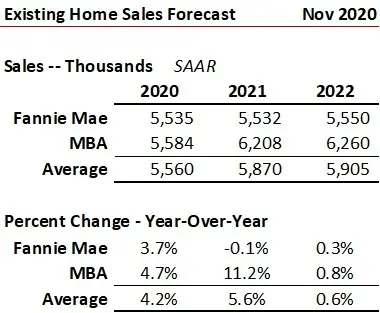

Housing makes up an estimated 15 percent to 18 percent of U.S. GDP according to the National Association of Homebuilders (NAHB) and has been a key contributor to the ongoing economic recovery in the pandemic. Existing home sales through September 2020, the latest data available as reported by the National Association of Realtors® (NAR), are shown in the graph, with the line representing total number of monthly sales on a trailing 12-month basis (TTM). The recovery from the plunge in sales in almost back to the pre-virus level.

The forecast from Fannie Mae and the MBA for existing home sales for 2021 and 2022 are shown in the table. Similar to interest rates, Fannie Mae expects home sales to essentially stay flat in 2021 while the MBA nods to gains – but the difference is large. The MBA forecasts double digit growth of 11.2 percent with sales rising to 6.208 million homes in 2021 from 5.584 million in 2020. At this point both expect little change from their respective sales forecasts from 2021 to 2022. NAR’s latest forecast calls for a 7.8 percent rise in existing home sales in 2021 to 5.86 million from 5.40 million in 2020.

Median price forecasts also differ with Fannie Mae forecasting the greatest median price gain in 2021 at 4.1 percent and the MBA just 1.1 percent.

New Home Sales and Median Prices

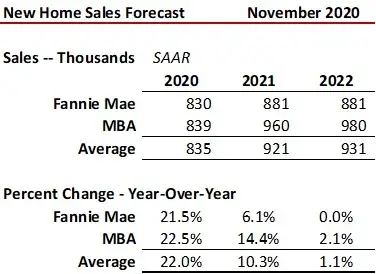

The forecast for new home sales is shown in the table. Both expect rising new home sales in 2021, but with the MBA at more than double that at 14.4 percent versus Fannie Mae’s 6.1 percent. Be aware there is a material difference in how new and existing home sales are reported. Existing home sales are actual closings where the ownership transfers while new home sales are merely signed purchase contracts that may not even have a building permit issued yet for construction. As a result, the restatement of new home sales each month can be large compared to minimal changes in existing home sales.

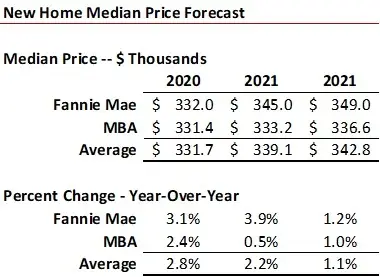

Just as with existing home price gains, Fannie Mae is looking at a greater 2021 increase in median new-home price at 3.9 percent compared to an almost zero 0.5 percent change by the MBA.

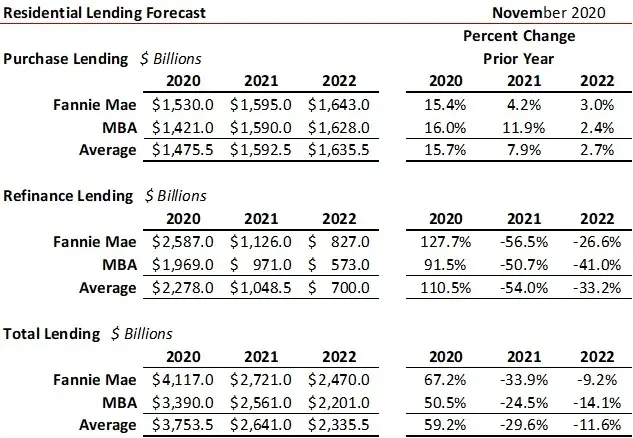

Residential Lending

After an all-time record level of residential lending in 2020, expectations are for a halving of refinance volumes in 2021 as interest rates elevate. Both Fannie Mae and the MBA see the same level of purchase lending in 2021 and 2022 at this time.

Epilogue

It is interesting that the MBA forecasts the largest gain in existing home sales in 2021 (up 11.2 percent) yet they also expect the biggest increase in residential mortgage rates rising to 3.3 percent – 50 basis points greater than Fannie Mae’s 2.8 percent average for the year. Logically, a rise in rates would spur home sales, so other factors must be in play.