Housing Market & Residential Lending Forecast Summary - June 2021

While forecasts from truly respected institutions are valued, unfortunately there is not always agreement from the various parties. The following summarizes monthly forecasts from Fannie Mae and the MBA.

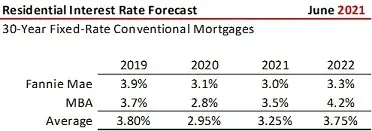

A critical foundation component for forecasting housing and residential lending is interest rates. Right out of the chute, Fannie Mae and the MBA see differing outcomes as shown in the table. Fannie Mae sees 30-year fixed conventional mortgage rates down 10 basis points (bp) this year and up 30 bp in 2022. The MBA, however, is forecasting a 70 bp gain for each this year and next.

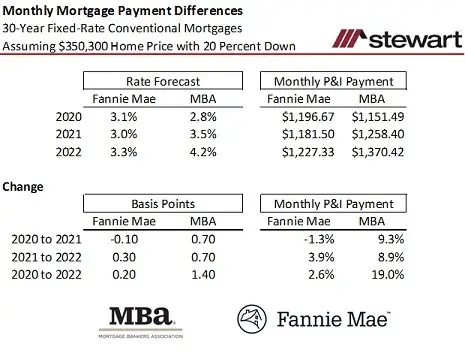

This is a material difference. Using the $350,300 median price of existing home sales in May 2021 as reported by the National Association of Realtors® and assuming a 20 percent down payment, monthly payments from 2020 through 2022 using the interest rate forecasts from Fannie and the MBA ranged from a low of $1,151.49 to a $1,370.40 high – an increase of 19.0 percent as shown in the second table below.

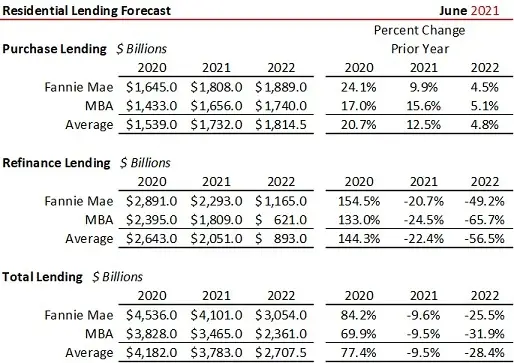

What is agreed on is a significant decline in refinance lending volumes. The next table shows the expectations for purchase, refinance and combined lending volumes. While the two forecasters see purchase lending up from roughly 10 to 16 percent in 2021 and around 5 percent in 2022, refinance lending is to shrink from 21 to 25 percent in 2021 and plunge an average 50 to 66 percent in 2022 as interest rates rise. Expectations are for total lending to drop 10 percent in 2021 and another almost 30 percent in 2022 with the drop all a function of disappearing refis.

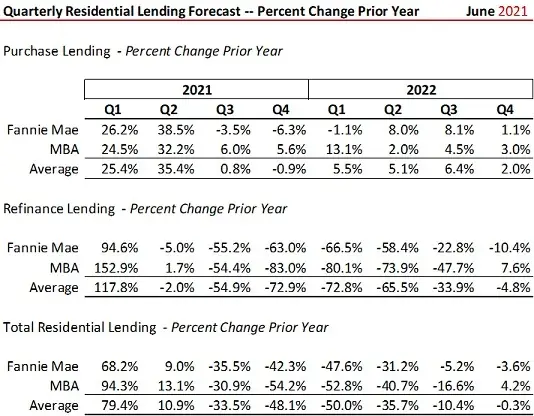

The next table shows the expectations for percentage changes quarterly for refis, purchase and total lending.

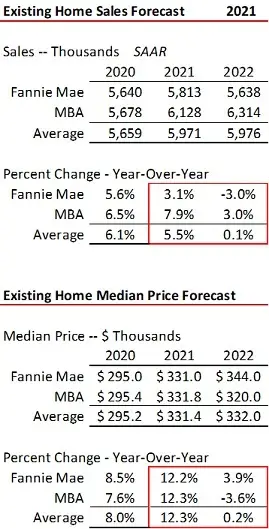

Both parties see a growing existing home market in 2021. Fannie Mae, however expects existing home sales to drop 3.0 percent in 2022 while the MBA sees a 3.0 percent gain. Concerning median prices, both now are projecting a 12+ percent gain in 2021. For 2022, however, Fannie Mae sees prices rising approximately 4 percent and the MBA down almost 4 percent. The difference is logical given the expectation by Fannie Mae for rates to rise only slightly and the MBA portending a material increase.

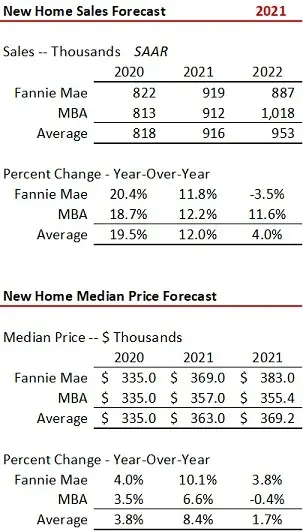

New home sales forecasts are similar to existing home sales expectations, as shown in the last table again with a similar divergence in 2022. Growth of new homes is constrained by low lot inventories, minimal skilled labor in roofing, framing, electrical and plumbing and supply-stream constrictions on materials – particularly in appliances and HVAC systems. While lumber costs remain highly elevated compared to April 2020, futures prices last week fell 43.8 percent from the high recorded in May of this year, but are still 200 percent greater than the $303.50 price per thousand board feet seen at the start of the pandemic in March 2020.

As shown, even the experts differ on where housing markets are heading, but agree on a declining refinance lending segment this year and next.

Following interest rates is the key to where the housing and lending markets are heading.