Plunging 2022 Residential Lending Volume — Housing Market & Residential Lending Forecast October 2021

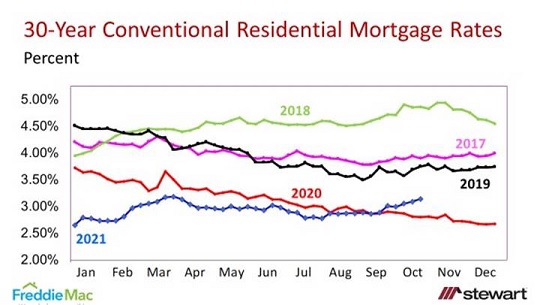

The summary of the latest monthly forecasts of residential housing markets and lending from Fannie Mae and the MBA are detailed in this blog. Interest rates are an integral component of housing sales and residential lending and popped up into the 3 percent range the last week of September, dipped to 2.99 percent the first of week of October then rose weekly during the month from 3.05 percent to 3.14 percent at month’s end – the highest rates seen since June 2020. The graph below shows conventional, fixed-rate 30-year mortgage rates as reported by Freddie Mac in their weekly Primary Mortgage Market Survey.

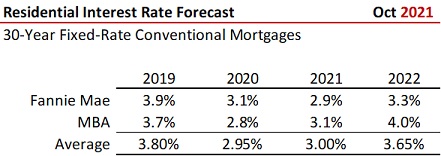

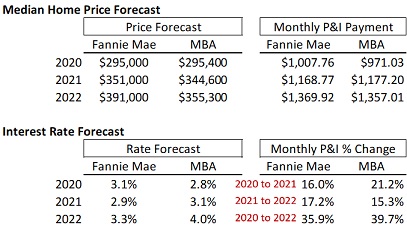

The latest interest rate forecasts from Fannie Mae and the MBA are shown in the first table. Fannie Mae continues to be more optimistic regarding 2022 with a 3.3 percent average rate while the MBA sees rates increasing from an average 3.1 percent in 2021 to 4.0 percent.

Existing Home Sales

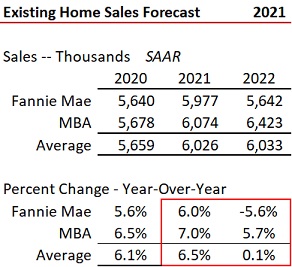

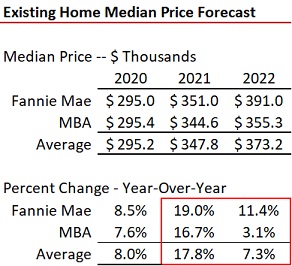

Existing home sales forecasts on a seasonally adjusted annualized rate (SAAR) and median price expectations are shown in the next two tables. Both Fannie Mae and the MBA each see sales rising in 2021 in a relatively tight range from 6.0 to 7.0 percent. They diverge, however, in 2022 with MBA calling for a 5.7 percent gain in existing home sales and Fannie Mae expecting a 5.6 percent decline. Both see strong price gains in 2021 (16.7 percent to 19.0 percent), but Fannie Mae (with a lower interest rate forecast) sees median prices increasing another 11.4 percent in 2022 while the MBA (with a greater interest rate forecast) sees median prices growing just 3.1 percent.

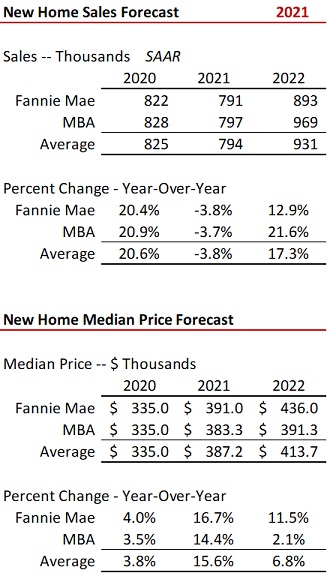

New Home Sales and Median Prices

The MBA continues to be more optimistic regarding new home sales with an expectation of 969,000 in 2022 versus Fannie Mae’s 893,000. Builder headwinds of skilled-labor shortages, lack of materials availability, rising input costs and minimal lot supply remain in place hindering growth in new construction. Just as with existing home median prices, Fannie Mae is much more bullish on new home price gains in 2022 (+11.5 percent) compared to the MBA’s +2.1 percent.

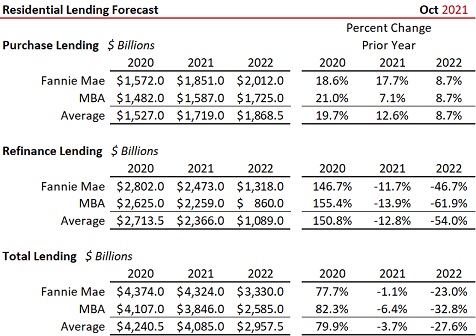

Residential Lending

Lending forecasts are detailed for both purchase and refinance transactions in the table. The story is the massive 47 percent to 62 percent plunge in refinance volumes in 2022, respectively, from Fannie Mae and the MBA. Purchase lending is expected to rise 12.6 percent (average) in 2021 and 8.7 percent in 2022.

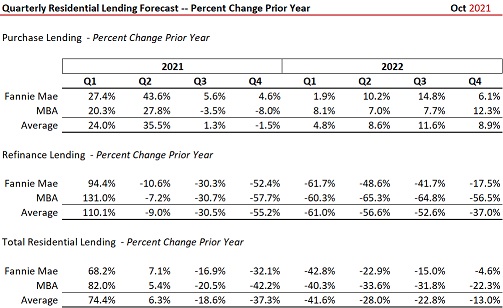

The next table shows the expected percentage change in lending volumes year-over-year on a quarterly basis. Total lending (purchase plus refinance) starts to precipitously decline in Q4 2021 (down 37.3 percent average) with a massive 41.6 percent plunge in Q1 2022 on a year-over-year basis. All of the decline is driven by quickly retracting refinance lending volumes.

The last table combines the median price and interest rate forecasts and shows the respective principal and interest payment (P&I) assuming 20 percent down. The estimates call for P&I monthly payment to increase in a range from 35.9 percent (Fannie Mae) and 39.7 percent (MBA) from 2020 to 2022, a significant and material decline in housing affordability.

To view and download these forecasts, click the following links:

https://www.fanniemae.com/research-and-insights/forecast/forecast-monthly-archivehttps://www.mba.org/news-research-and-resources/research-and-economics/forecasts-and-commentary/mortgage-finance-forecast-archives

The latest weekly interest rate data from Freddie Mac can be found at:

http://www.freddiemac.com/pmms/

As stated in this blog for almost one-half a year:

“As shown, even the experts differ on where housing markets are heading, but agree on a declining refinance lending segment this year and next. Following interest rates is the key to where the housing and lending markets are heading.”

This massive head-on collision on affordability (with projected P&I payments increasing from 35.9 percent to 39.7 percent from 2020 to 2022) remains my greatest long-term concern for the economy and wealth-building for households. In 2019 (latest data available) houseowner’s primary dwelling equity made up 26 percent of all U.S. household net worth according to the Survey of Consumer Finances conducted by the Federal Reserve. If housing is removed from the investment equation due to affordability, then those households will not participate in what historically has been one of the largest stores of wealth for middle-class America.

Ted