Interest Rate Uncertainty Leaves Housing Trajectory in Question

Fannie Mae & MBA Latest Housing & Residential Forecasts November 2022

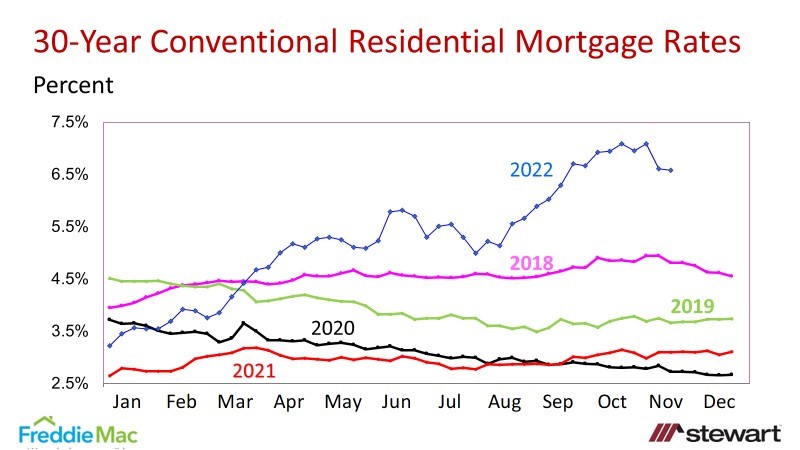

Since the onset of the COVID-fueled pandemic. the U.S. saw the lowest residential mortgage lending rates in history of 2.65 percent in January 2021 per Freddie Mac. Rates have since more than doubled due to inflation and the Federal Reserve’s actions to slow the economy.

Inflation continues as the key contributor to the shrinking outlook for housing sales and residential lending as it drives interest and borrowing rates upwards. Despite a fourth 75 basis point hike in the target for the Fed Funds Rate (the rate at which a bank can borrower necessary overnight reserves from other banks) the Fed continues to shape expectations for more increases in coming months. The goal is to slow the economy and shrink inflation that is persisting at near 40-year highs, 7.7 percent based on the Consumer Price Index. The Federal Reserve’s favorite measure of inflation is the Personal Consumption Price Index (PCE), a broader measure of the costs of goods and services purchased by consumers. The PCE was up 6.2 percent in the 12-months ending September 2022 -- unchanged from the prior month. Core PCE (which excludes the volatile costs of food and energy) rose from 4.9 percent in August to 5.1 percent as of September. The 40-year Core PCE rate was 5.4 percent in February of this year – a four-decade high.

Conventional 30-year fixed-rate mortgage rates are shown in the following graph as reported by Freddie Mac in their weekly Primary Mortgage Market Survey (PMMS). The PMMS is now based on weekly loan applications from thousands of lenders across the country as of November 2022. Prior to this it was a weekly survey of lenders by Freddie Mac. The latest rate (November 23, 2022) was 6.58 percent – down from 7.08 percent two weeks ago which was the highest seen in 20 years.

Interest Rate Expectations

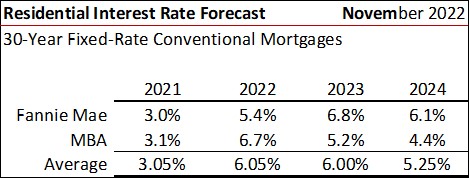

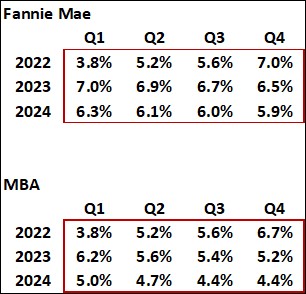

Residential expectations remain divergent between Fannie Mae and the MBA’s expectations as shown in the tables below. The first table shows annual rates and the next quarterly. While the MBA sees annual rates declining from 2022 to 2023 (going from 6.7 percent to 5.2 percent), Fannie Mae is projecting a 140 basis point increase in annual rates rising from 5.4 percent in 2022 to 6.8 percent in 2023..

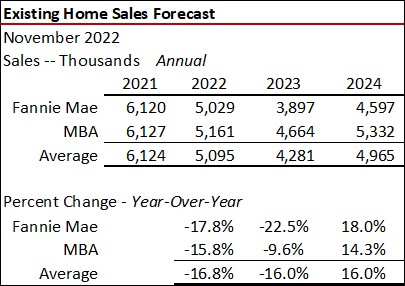

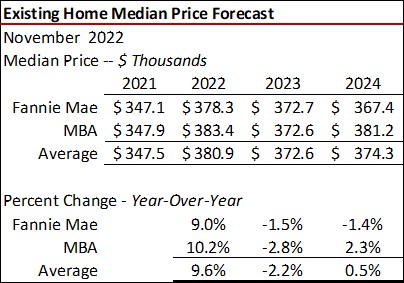

Existing Home Sales & Median Prices

Both Fannie Mae and MBA forecast declining existing home sales in 2023. Fannie Mae, however, sees sales plunging to the lowest level seen since 1995, down 22.5 percent year-over-year to 3.9 million units. The MBA expects 4.7 million existing home sales which would be down 9.6 percent from 2022.

The two are similar in their forecasts of median prices, dipping from 1.5 percent to 2.8 in 2023. My personal forecast calls for median prices to dip from 10 percent to 12 percent in 2023 Vs 2022 due to an eroding economy, high rates and affordability issues.

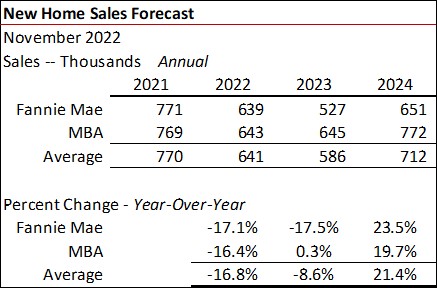

New Home Sales

Since 2002, there has been an average one new home sale for every 8.9 existing home closings. Fannie Mae, given the expectation of much higher interest rates, forecasts new home sales to drop 17.5 percent in 2023 compared to MBA’s essentially flat sales outlook (+0.3 percent). Both see an approximate 20 percent gain in new home sales in in 2024.

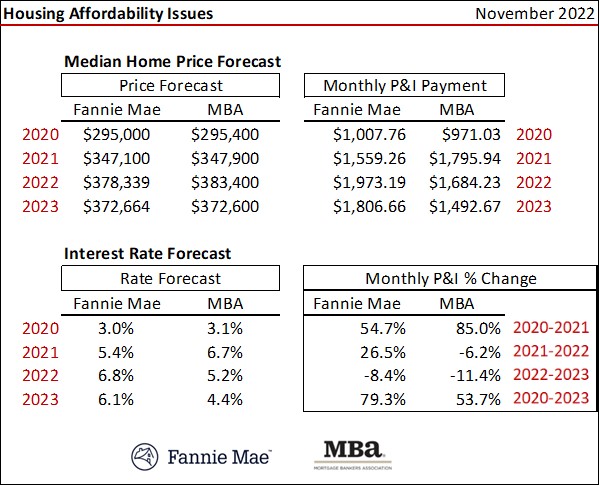

Monthly Principal & Interest Payments 2020 Vs 2023

Known is the typical principal & interest payment (P&I) in 2020 for the median priced-home at the average annual interest rate. If the MBA is correct in their current 2023 forecast, the typical P&I payment will be 53.7 percent greater compared to 2020. If Fannie Mae is on target, the monthly P&I payment in 2023 will be up 79.3 percent Vs 2020. The increase in P&I is a function of changes in median price and interest rates.

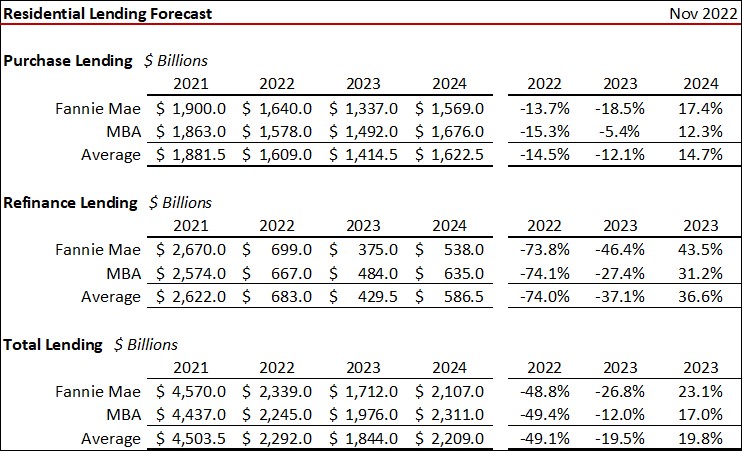

Residential Lending

Rising interest rates crushed refinance activity in 2022 compared to 2021 (down a projected 74 percent) with another 31.2 percent to 43.5 percent drop in 2023. More than one-half of all residential mortgage lenders in business in 2021 are now out of a job in the mortgage industry with more cuts yet to come.

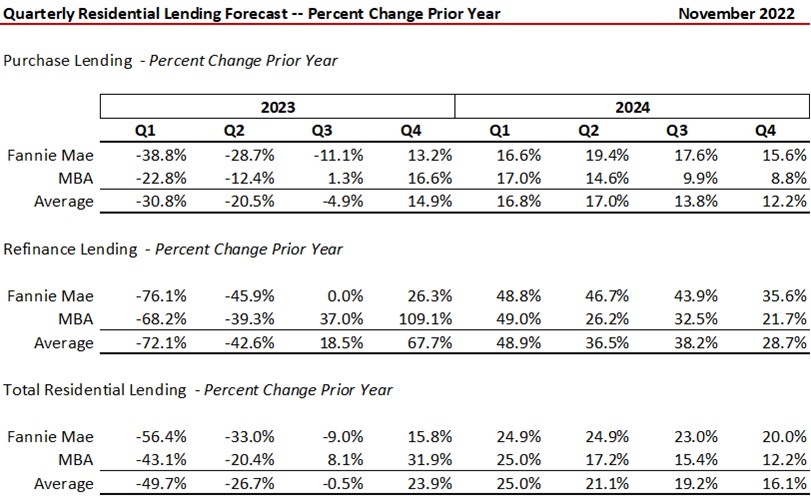

The chart below shows quarterly year-over-year lending changes for purchase and refinance activity. If correct, there is material pain still coming through the first two quarters of 2023 in the residential lending segment and residential brokerages.

The outlook can change and will be a function of interest rates, whether a material recession takes place, consumer confidence and inflation. The U.S. Congress Joint Economic Committee estimates that inflation is costing the typical household in the country $728 more per month to maintain their lifestyle compared to one year ago. At Freddie Mac’s current 6.58 percent mortgage rate, the typical household lost a massive $114,200 of loan capacity to purchase a home assuming no change in income.

Interest rates, jobs, consumer confidence (recession expectations) are keys to the trajectory of the economy and housing. Stay focused on these metrics.