U.S. Existing Home Sales Down 22.4 Percent Year-Over-Year in July 2022 - With No Relief In Sight ...

For most Americans the home is their largest store of wealth. The leading indicator of the health of housing market is the number of sales – not median price. The first indicator of a softening housing market is a drop in sales. Initially as sales decline, median prices continue to rise, Eventually, however, if sales shrink enough and supply increases, prices then decline.

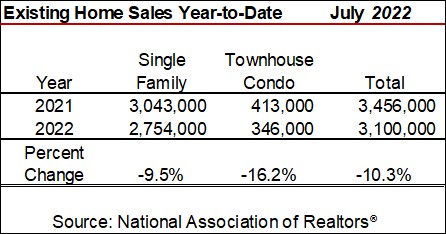

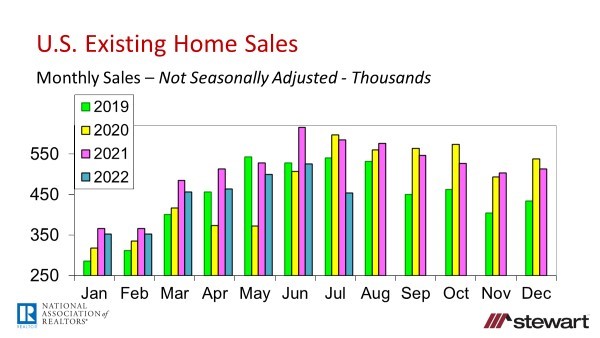

Existing home sales dropped 22.4 percent in July 2022 to 453,000 versus July 2021 (on a raw, unadjusted basis) according to the National Association of Realtors® and were down 20.2 percent on a seasonally adjusted annualized rate (SAAR) to 4.18 million. Sales have now declined six consecutive months on a SAAR. Year-to-date existing home sales are down 10.3 percent from the same period a year ago – a decline that is accelerating.

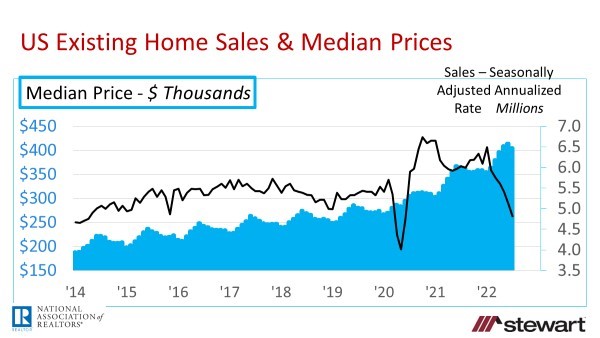

Median price rose 10.8 percent year-over-year to $403,800, but was down from the June 2022 record high of $413,800. Median prices have increased 125 consecutive months – the longest upside streak ever recorded.

Box Score -- Existing Home Sales July 2022 National Association of Realtors® (NAR)

Monthly Sales _– raw data not seasonally adjusted_ 453,000 for the month of July 2022

down 13.7 percent sequentially versus the 525,000 sales in June 2022

down 22.4 percent year-over-year versus the 584,000 sales in July 2021

Seasonally Adjusted Annualized Sales Numbers (SAAR)

4.81 million SAAR as of July 2022

down 5.9 percent sequentially from June 2022 sales of 5.11 million

down 20.2% percent year-over-year from 6.03 million in July 2021

Sales Trailing 12-Months _– raw data not seasonally adjusted_

5.764 million for the 12-months ending July 2022 _– raw data not seasonally adjusted_ down 2.2 percent vs 12-months ending June 2022 of 5.895 million

down 6.8 percent vs 12-months ending July 2021 of 6.183 million

Sales Year-to-Date _– raw data not seasonally adjusted_

Median Price – July 2022 _due to historic monthly seasonality of existing home prices, only a year-over-year comparison is made_

$403,800 – _not seasonally adjusted_ up 10.8 percent vs $364,000 July 2021

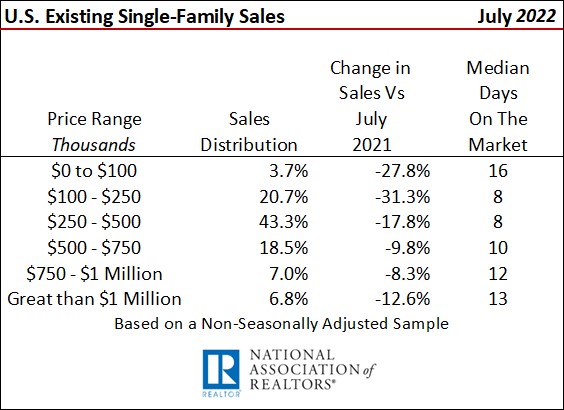

Single-Family Sales by Price and Median Days on the Market Prior to an Accepted Purchase Contract

For the first time since May 2020, sales were down year-over-year in each and every price range.

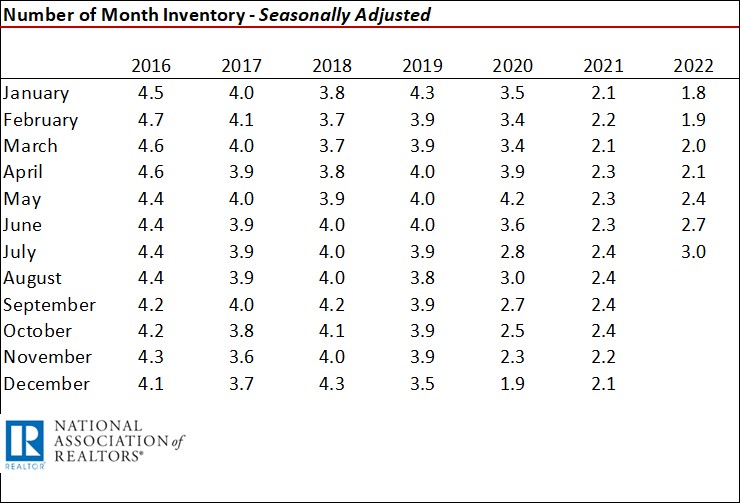

Months Inventory – with 6.0 months inventory considered normal from a historical perspective – _Seasonally Adjusted_

Graphs

The seasonally adjusted annualized sales rate of 4.81 million in July 2022 was the lowest seen since June 2020. To reach a lower historical number (excluding the initial months of the pandemic) requires going back to April 2014.

Note that July 2022 sales were less than July 2019 – the year prior to the pandemic.

Other Details Included in the NAR July 2022 Release

Inventory rose 4.8 percent from June 2022 with 1.31 million active listings but was unchanged from the prior year

Months Inventory at the end of July 2022 was 3.3 months (not seasonally adjusted) compared to 2.6 months 1-year ago

Typical property was on the market 14 days prior to an accepted purchase contract versus 17 days one-year ago

82 percent of homes closed in July 2022 were on the market less than one month before going under contract

1st time homebuyers accounted for 29 percent of July closings, almost flat from 30 percent one-year ago. Continuing erosion of affordability will no doubt negatively impact 1st-time homebuyers ability to access the great American dream given rising prices and interest rates

Investors purchased 14 percent of the homes sold in July 2022 versus 15 percent in the same month last year

Buyers paid all-cash in one-in-every-four sales (24 percent) almost the same as 23 percent one-year ago

Distressed sales – foreclosures and short sales – are still not an issue, making up 1 percent of July 2022 transactions. This was unchanged from the prior month & year-over-year. Most homeowners unable to make their mortgage payments today merely need to list the property with a real estate agent and prepare to walk with equity from a closing sometime in the next 30 to 90 days provided the property is appropriately priced and prepared for sale. If the property is not properly priced given rising inventory, it will languish on the sidelines

To read the full press release from NAR click here.

Economic conditions (inflation) and challenging affordability now control the destiny of the U.S. housing market.

Inflation - Recent months have seen the highest inflation rate in 40 years which peaked at 9.1 percent in June and cooled only slightly to 8.5 percent in July. The US Congress Joint Economic Committee estimated current inflation is costing households $635 per month. At the now 5.13 percent 30-year conventional mortgage rate, a monthly payment of $635 would service a $116,557 loan. Conventional 30-year fixed-rate mortgage rates have doubled from the all-time record low of 2.65 percent in January 2021.

Recession – Each of the past 10 recessions were defined by two or more consecutive quarters of negative Gross Domestic Product (GDP). Q1 1 and Q2 GDP this year came in-1.6 percent and -0.8 percent, respectively. Even if Washington, D.C. continues to say there is no recession, consumers actions will dictate whether there will be one or not. Retail sales typically make 70 percent of GDP. As consumers anticipate a downturn they buy less which causes the recession.

Affordability – If the current forecasts from Fannie Mae and the MBA are correct for median home prices and interest rates in 2023, the monthly principal and interest payment for a household buying the typical home will increase from 2020 to 2023 by 70.4 percent to 81.2 percent.

Follow me on Twitter at https://twitter.com/DrTCJ

There is nothing on the economic radar to indicate that the shrinking home sales trend will change in the next 12 to 18 months.

Ted