Q1 2020 Commercial Real Estate Market Cycle Report -- A Baseline or Highwater Mark for Now

Dr Glenn Mueller’s Q1 2020 Real Estate Market Cycle Report just arrived. Under normal circumstances, this timely report allows the latest purview in just eight pages of 54 commercial markets across the country for apartment, Industrial, office, and retail properties. Now, given the massive economic erosion in many markets across the country since the second-half of March 2020, this report is simply going to serve today as the highwater mark or new baseline for markets for the near future – at least until economic activity returns to a more normal level.

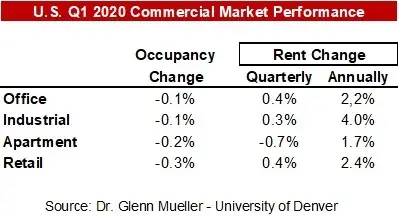

Findings as of Q1 2020:

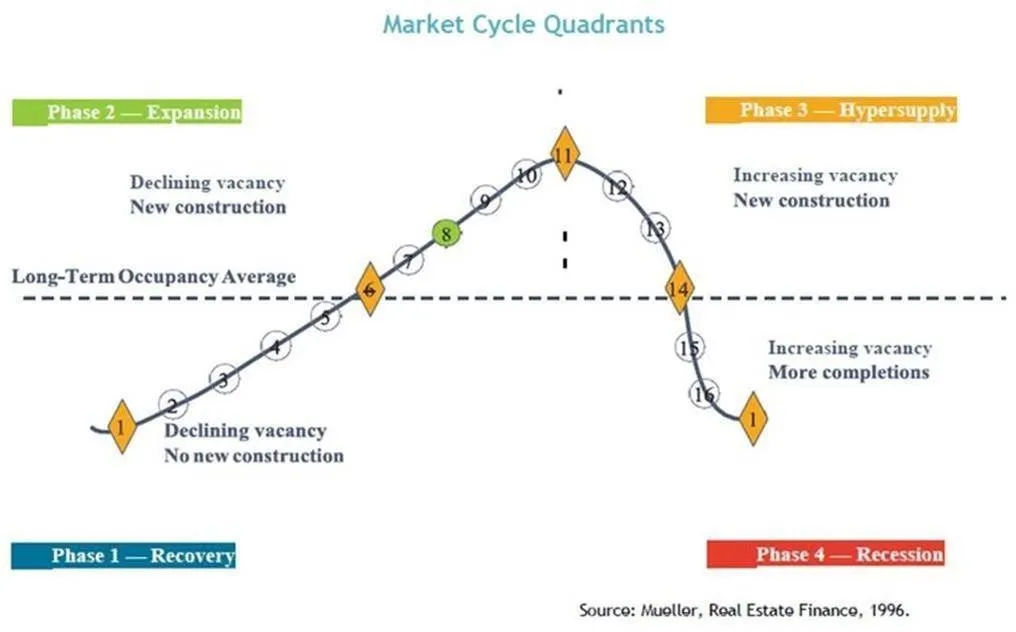

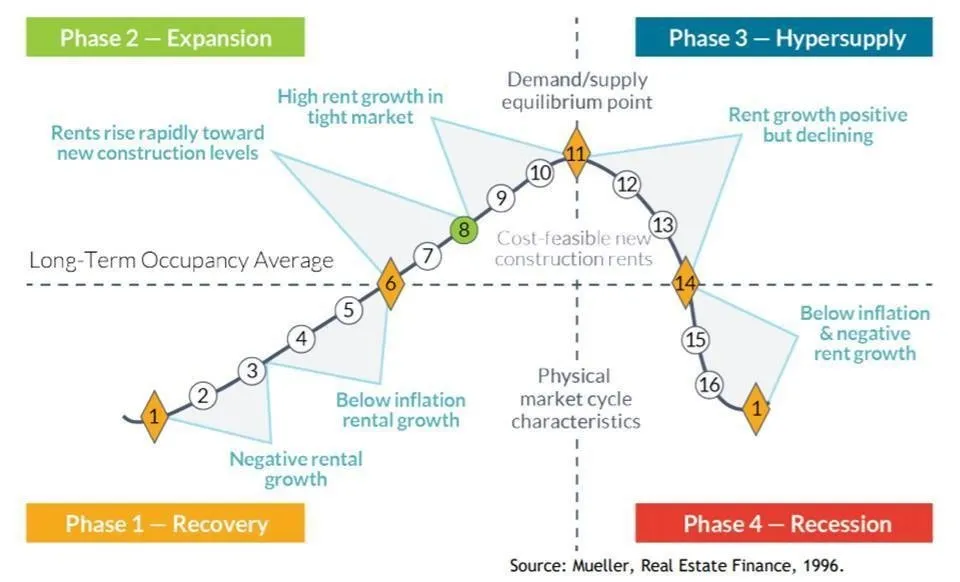

Dr. Mueller defines four distinct phases in the commercial real estate cycle providing decision points for investment and exit strategies. Long-term occupancy average is the key determinant of rental growth rates and ultimately property value. Ideally, Phase 2 is the sweet-spot for real estate investor performance.

Across the cycle, Dr. Mueller has described rental behavior within each of the phases, using market levels ranging from 1 to 16. The equilibrium market level is 11, where neither demand nor supply drive rent changes. This is also the peak occupancy level.

Recovery _Declining Vacancy, No New Construction_

1-3 Negative Rental Growth

3-6 Below Inflation Rental Growth

Expansion _Declining Vacancy, New Construction_

6-8 Rents Rise Rapidly Toward New Construction Levels

8-11 High Rent Growth in Tight Market

Hypersupply _Increasing Vacancy, New Construction_

11-14 Rent Growth Positive But Declining

Recession _Increasing Vacancy, More Completions_

14-16, then back to 1 Below Inflation, Negative Rent Growth

These are illustrated in the following graphic from Dr Mueller’s report.

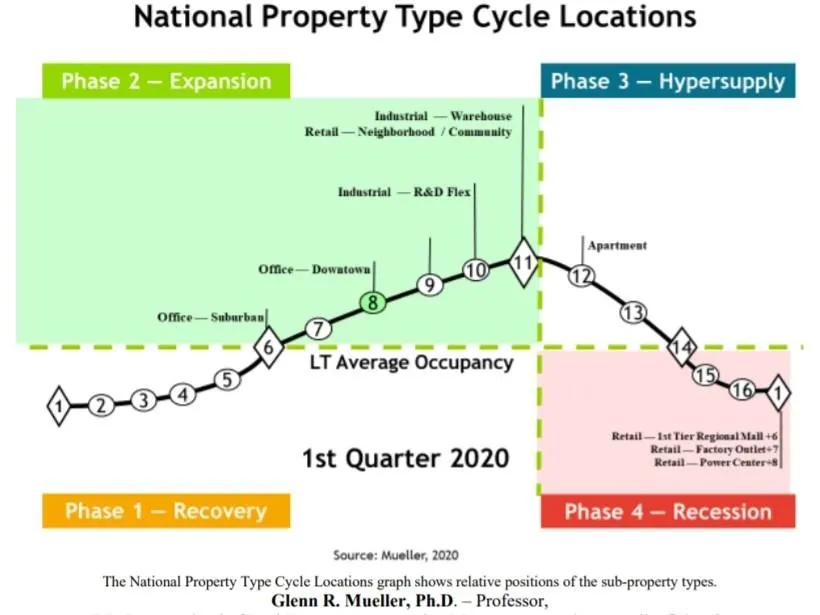

The following graph from Dr. Mueller’s Q1 2020 report shows the current cycle stage from a national perspective. Apartments, with ongoing new deliveries in the past six years and a pipeline of construction, are the most mature property type across the cycle and are in the Hypersupply Phase with rents still increasing but at a declining rate. Industrial property is now the big winner along with Retail—Neighborhood/Community (think your local neighborhood retail center anchored by the grocery store). Three Retail Property Types now reside at or near the bottom scale of Phase 4- Recession: 1st Tier Regional Malls, Factory Outlet Centers and Power Centers.

The following table shows the 54 markets for Industrial properties. The Coronavirus may have expedited the demise of retail, but to the benefit of industrial properties as everything ordered online and not shipped from a retail storefront comes from an industrial property. Likewise, more and more manufacturing is being and is going to be done in the U.S. as critical sourcing and manufacturing is likely shifted away from China. Two metros moved into the Hypersupply Phase in Q1 2020 denoted by the +1 suffix – Austin and Los Angeles. Two other metros moved one notch further into Hypersupply, going from 12 to 13 – East Bay and Houston.

Pay attention to each of the property types in the report focusing on cities that have excess supply, and also those with supply trailing demand. To read the entire report and view the findings for all property types see the following download information.

To download historical quarterly reports click https://daniels.du.edu/burns-school/ and scroll down to the REAL ESTATE MARKET CYCLE REPORT section on the Website. For the Q1 2020 click https://daniels.du.edu/assets/Cycle-Monitor-19Q4.pdf

To learn more about Dr Glenn Mueller click https://daniels.du.edu/directory/glenn-mueller/

Ted