Existing Home Sales Continue to Struggle in May 2023

Down 20.4 Percent & Median Price Off 3.1 Percent Year-Over-Year

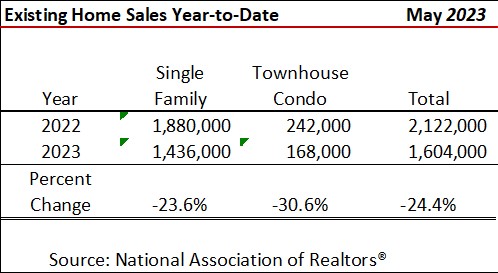

Existing home sales on a seasonally adjusted annualized rate (SAAR) came in 20.4 percent short year-over-year in May 2023 along with median prices off 3.1 percent on a nominal basis (not adjusted for inflation) according to the National Association of Realtors® (NAR). Year-over-year sales have now declined for a record 21-consecutive months on a SAAR. Sales year-to-date were down 24.4 percent overall with single family off 23.6 percent and condo-townhouse sales plunging 30.6 percent. The number of months of inventory remained unchanged at 2.8 months for the third month in a row on a seasonally adjusted basis.

Box Score -- Existing Home Sales May 2023 National Association of Realtors® (NAR)

Monthly Sales – raw data not seasonally adjusted

408,000 for the month of May 2023

up 21.1 percent sequentially from 337,000 sales in April 2023 -

down 18.2 percent year-over-year versus the 499,000 sales in May 2022

Seasonally Adjusted Annualized Sales Numbers (SAAR)

4.3 million SAAR as of May 2023 – the fewest sales in May since 2020 notched at the onset of the pandemic

Essentially flat (up 0.2 percent) sequentially from April sales of 4.29 million

down 20.4 percent year-over-year from 5.40 million in May 2022

Sales Trailing 12-Months – raw data not seasonally adjusted

4.51 million for the 12-months ending May 2023 – raw data not seasonally adjusted

down 24.7 percent vs 12-months ending May 2022 of 5.99 million

down 2.0 percent sequentially from April 2023 of 4.60 million

Sales Year-to-Date – raw data not seasonally adjusted

Median Price – May 2023 due to historic monthly seasonality of existing home prices, only a year-over-year comparison is made

$396,100 – not seasonally adjusted

down 3.1 percent vs $408,600 May 2022

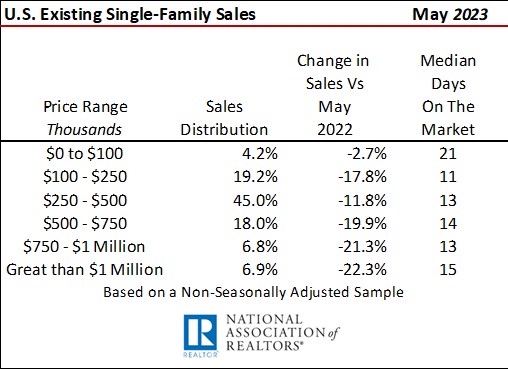

Single-Family Sales by Price and Median Days on the Market Prior to an Accepted Purchase Contract

Months Inventory – Seasonally Adjusted

Prior to the pandemic, 6 months of inventory for existing homes was considered normal. I do believe, however, with the full integration of online home searches and technologies such as virtual home tours, digital signatures and closing aids such as remote online notarizations, the new normal is one-half the pre-pandemic levels. Thus I would argue that the U.S. overall now is normal in the relative number of listings. The number of months of inventory is not a factor in reduced May home sales as January 2022 saw 1.8 months inventory with closings at 6.49 million on a SAAR.

Graphs

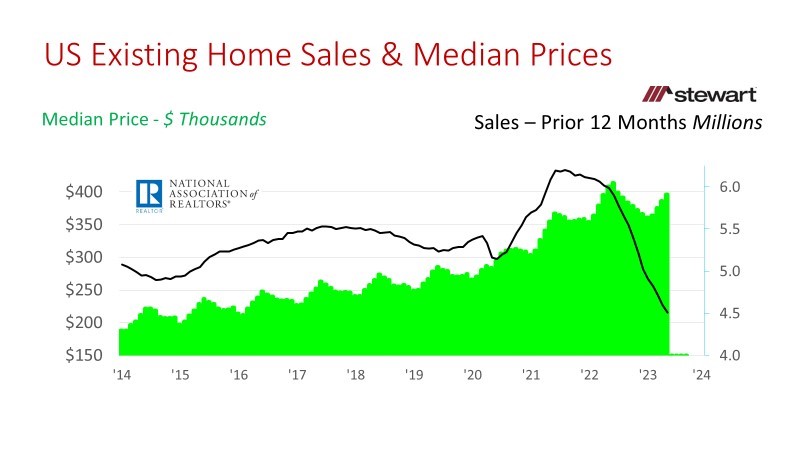

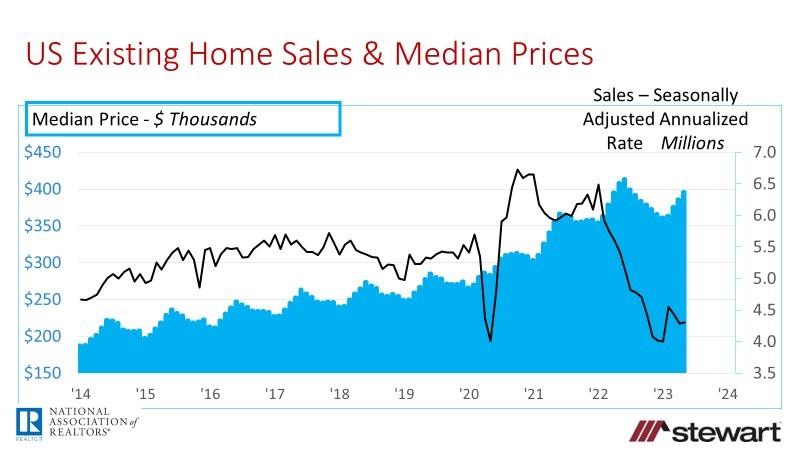

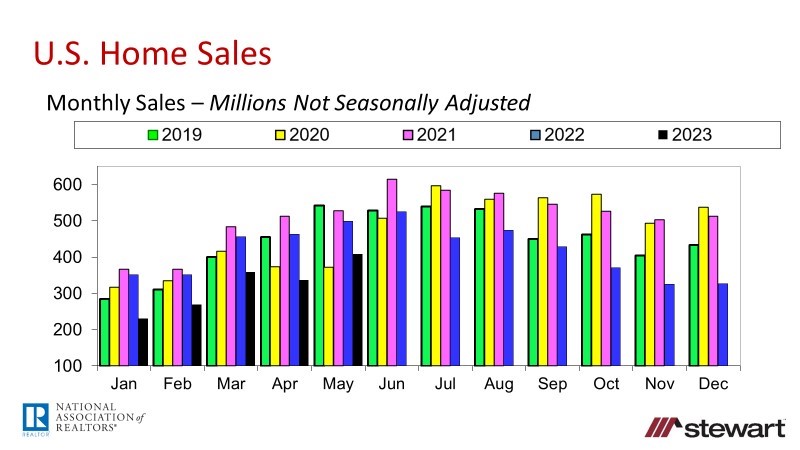

The next graph shows the raw, unadjusted number of monthly home sales annually from 2019 through May 2023. The real comparison is not monthly 2023 sales numbers to 2020, 2021 or 2022 as these data are anomalies due to the pandemic. The only time look at 2020, 2021 and 2022 data in the future will be in the next pandemic to serve as a gauge in forecasting sales and market behaviors at that time. Since the last normal market was 2019, comparison of 2023 data should be made to that year. Sales in 2023 compared to 2019 have dropped for five consecutive months sequentially. The erosion in monthly home sales comparing 2019 to 2023 has been -18.9 percent in January, -13.5 percent in February , -10.3 percent in March, -26.1 percent in April and -24.7 percent in May.

Other Details Included in the NAR November 2022 Release

Listing inventory of 1.08 million units in May 2023 was up 3.8 percent sequentially from April but down 6.1 percent compared one-year ago

Months Inventory at the end of May 2023 was 3.0 months (not seasonally adjusted) compared to 2.6 months in May 2022

Typical property was on the market 18 days prior to an accepted purchase contract versus 16 days one-year ago

Three-in-four of homes closed in May 2023 (74 percent) were on the market less than one month before going under contract

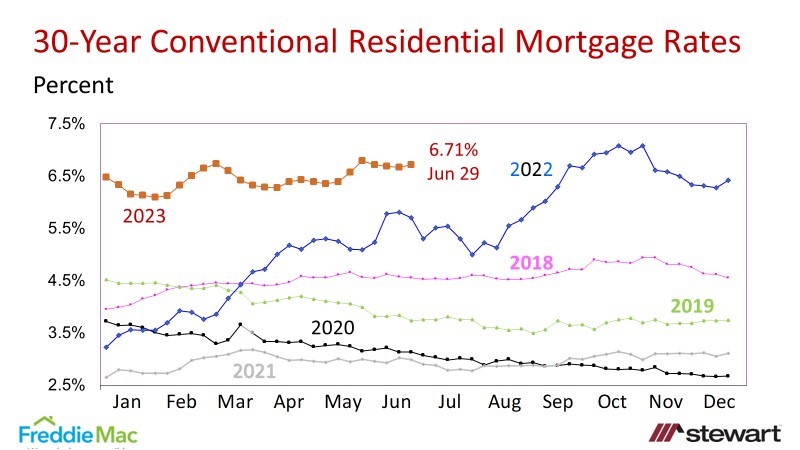

1st time homebuyers accounted for 28 percent of May closings, up slightly from 27 percent one-year ago. Continuing erosion of affordability will no doubt negatively impact 1st-time homebuyers ability to access the great American dream given rising prices and interest rates. Following is a weekly graph of 30-year conventional fixed-rate mortgages as reported by Freddie Mac’s weekly Primary Mortgage Market Survey (PMMS).

Investors purchased 15 percent of the homes sold in November 2022 versus 15 percent in the same month last year

Buyers paid all-cash in one-in-every-four sales (25 percent), unchanged from one-year ago

Distressed sales – foreclosures and short sales – remained at 2 percent of all closings

To read the full press release from NAR click here.

Economic conditions (inflation) and challenging affordability continue to control the destiny of the U.S. housing market.

Inflation - Conventional 30-year fixed-rate mortgage rates have more than doubled from the all-time record low of 2.65 percent in January 2021 and now are at 6.71 percent as of the end of June 2023.

Home Sales Pipeline – NAR Pending Home Sales May 2023 The just-released National Association of Realtors’ Pending Home Sales Index (newly signed home-purchase contracts) for May 2023 was down 22.2 percent compared to 1-year ago and down 2.7 percent sequentially from April. Pending home sales typically make up closings for the next 60 to 90 days.

Although NAR is forecasting 4.78 million existing home sales with stable prices in 2023, there continues to be nothing on the economic radar indicating the shrinking home sales trend will change significantly in the coming six to 12 months given median prices are down 3.1 percent year-over-year with 4.30 million home sales on a SAAR. In comparison, Fannie Mae anticipates 4.21 million existing home sales in 2023 with median price down 1.2 percent while the MBA sees 4.29 million sales with price down 4.6 percent.

Follow me on Twitter at https://twitter.com/DrTCJ

Ted