Forecasting Home Sales and Residential Lending Just Like the Weather: Continual Change and Uncertainty - Fannie Mae & MBA July 2023

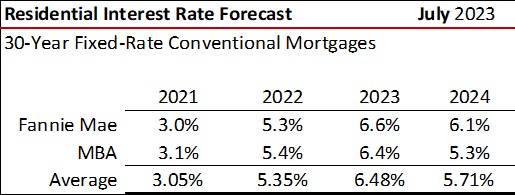

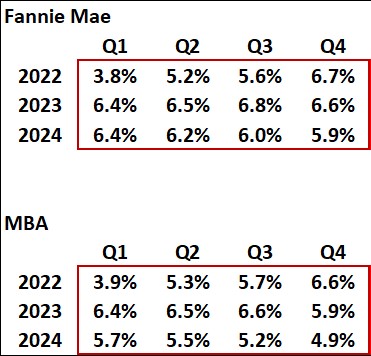

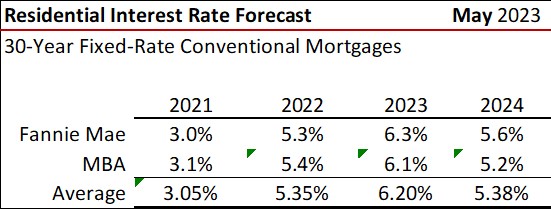

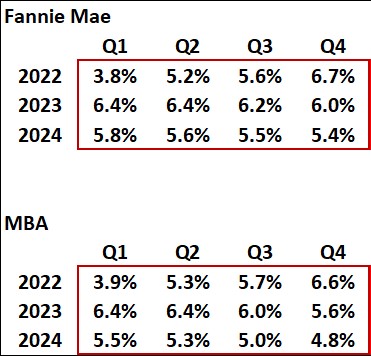

Residential mortgage rate expectations rose for the second month in a row in the July 2023 forecasts released by Fannie Mae and the MBA. The first set of tables shows 30-year conventional mortgage rate expectations as of July while the second set details forecasts from May, just two months ago. The MBA continues to expect lower rates sooner than Fannie Mae, but neither sees rates (on a quarterly average) slipping out of the 6 percent range until at least Q4 this year (MBA) with Fannie forecasting rates in the 6 percent range through the first quarter of 2024. On an annual basis, Fannie Mae expectations are 80 basis points greater than the MBA on average in 2024.

July 2023

May 2023

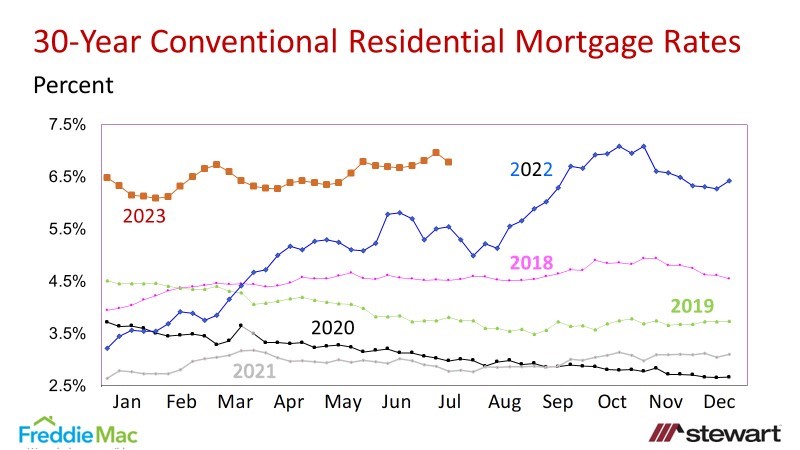

Residential mortgage interest rates are the compass for home sales and residential lending. Historical conventional 30-year fixed-rate mortgage rates are shown in the following graph as reported by Freddie Mac in their weekly Primary Mortgage Market Survey (PMMS). The latest rate as of the week ending July 20, 2023, was 6.78 percent, down from 6.96 percent the prior week and from 7.08 percent the last week of October 2022 which was the highest seen in past 20 years. Daily rates from other information sources continue to be quoted in the high 6 percent to low 7 percent range, however.

Existing Home Sales

Historical existing home sales from 2001 through 2022 are detailed in the next graph plus 2023 and 2024 forecasts from Fannie Mae and the MBA. Current estimates for 2023 call for the fewest existing home sales in the past 12 to 13 years. While the MBA anticipates a slight improvement in 2024, Fannie Mae sees no change. The MBA remains a bit more optimistic given their expectations for lower residential mortgage rates.

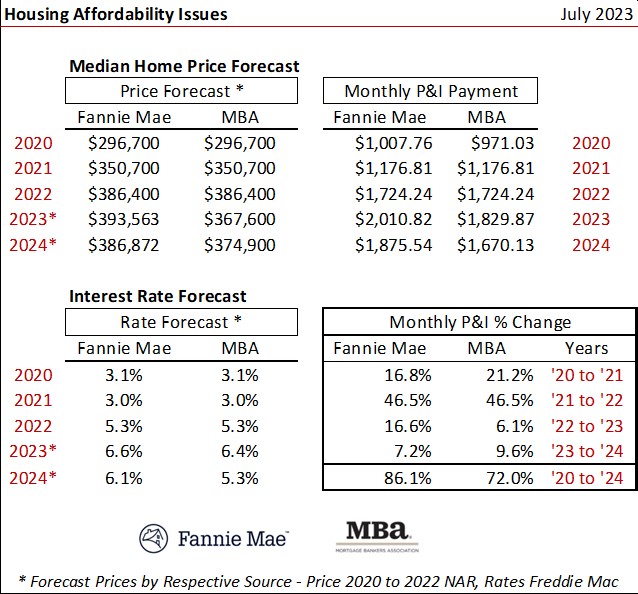

Existing home sales and median prices are tallied in these tables. Though the MBA expects a 4.3 percent decline in median prices in 2023, Fannie Mae forecasts a 3.9 percent gain. These expectations flip in 2024 with Fannie Mae calling for a 1.7 percent drop in median price and MBA seeing a 2.0 percent gain.

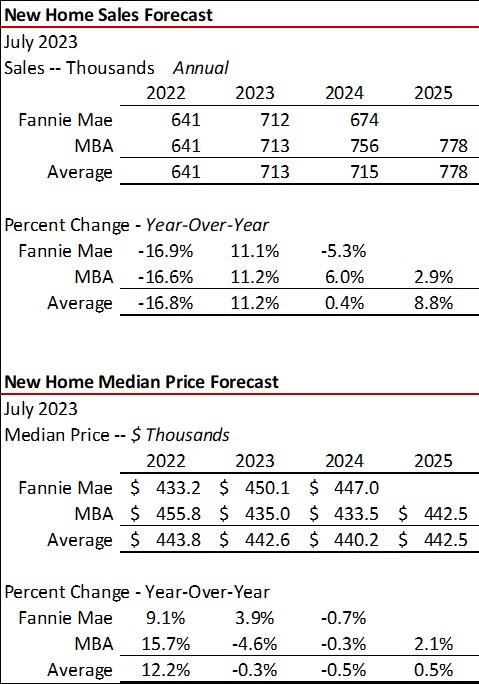

New Home Sales

Since 2002, there has been one new home sale for every 8.8 existing home closings on average. Current forecasts from Fannie Mae and the MBA call for new home sales to be up 11 percent in 2023. The two diverge for 2024, with MBA expecting a 6.0 percent rise in new home sales and Fannie Mae seeing a 5.3 percent decline.

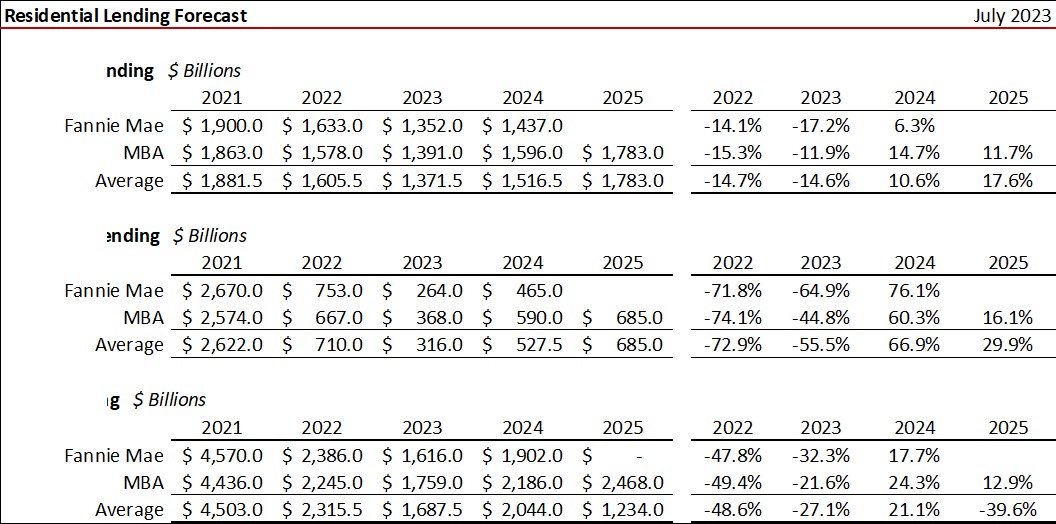

Residential Lending

Rising interest rates crushed refinance activity in 2022 compared to 2021 (down 73 percent) with another 50+ percent freefall (average) expected in 2023. More than 6-in-10 residential mortgage lending officers in business in 2021 are now out of a job in the mortgage industry. When the smoke from this implosion clears, for every 10 residential loan officers in business 2021 there will likely be just three by the end of 2023.

Estimated Mortgage Payments

The last table shows the typical monthly mortgage payment based on respective MBA and Fannie Mae forecasts assuming 20 percent down. The impact of rising rates and median home prices since 2020 compared to 2024 (forecast) will see monthly payments increase by 72 percent to 86 percent. Average hourly wage earnings, in comparison, rose by just 14.3 percent from June 2020 to June 2023. The massive drop in affordability is responsible for the plunge in home sales due to rising interest rates and home values.

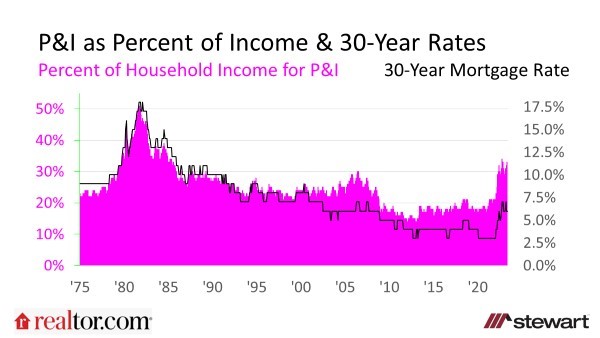

Affordability is not expected to improve much even if interest rates decline. Median price rise is the primary culprit impacting affordability. U.S. existing home median prices rocketed up from $294,400 in June 2020 to $410,200 as of June 2023 according to NAR – a gain of 39.3 percent. In May 2020, the typical household purchasing the median priced home would spend 18 percent of their household income on principal and interest payments assuming 20 percent down according to an analysis completed by Realtor.com. That rocketed up to 33 percent – almost double – as of May 2023, as shown in the graph.